Down payment on a house: How much should a house down payment be?

Table Of Content

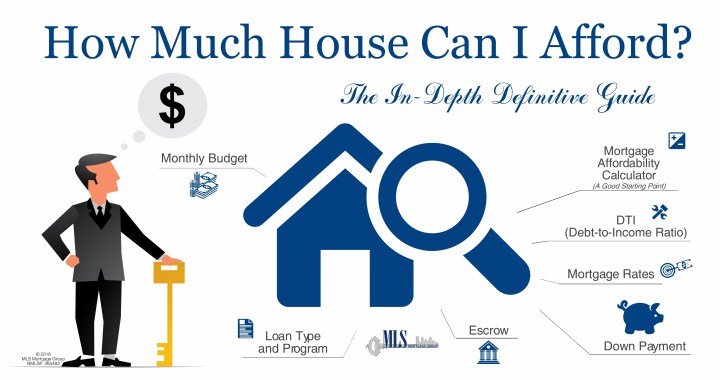

The average home buyer can typically expect to spend 2% – 6% of the home purchase price in closing costs, which includes inspections, appraisals and earnest money. Once you add these expenses to the purchase price, the total cost of buying a home starts to snowball. Your mortgage lender will calculate your debt-to-income ratio (DTI) to determine the maximum size of your loan. DTI measures how much of your gross monthly income you spend on debt. Lenders look at the money left over after your regular debts are paid to see how much you can afford for a monthly mortgage payment. If you have an FHA loan, you will almost certainly pay mortgage insurance, which includes a premium upfront and additional premiums built into your mortgage payment.

What is an excellent credit score?

You can also use a mortgage affordability calculator to ballpark your home price range. If you want to buy a house, you need to meet basic requirements for credit score, income, and employment history as well saving for a down payment. Exact guidelines will vary depending on the type of home loan you use.

How to Get Pre-Approved for a Home Loan

To buy a house, you’ll need a qualifying credit score and debt-to-income ratio, proof of income and employment, and enough cash to cover the down payment and closing costs. Specific qualifying requirements will vary depending on your loan program and mortgage lender. These are upfront cash payments that you make at closing for certain mortgage expenses before they’re actually due, including things like homeowners insurance, property taxes and mortgage interest.

How does the amount of my down payment impact how much house I can afford?

If you want to explore an FHA loan further, use our FHA mortgage calculator for more details. "This is especially true among first-time buyers, who have proven to be resilient over recent years, and now account for the largest proportion of homes purchased with a mortgage in almost 30 years." Disabled people could receive vouchers instead of monthly payments under proposed changes to Personal Independence Payment (PIP). Home prices have escalated in part because of a lack of available for-sale properties. Buying a home remains a primary wealth-building tool for U.S. households, but rising home prices have placed homeownership increasingly out of reach for the average American. To comfortably afford a typical home, Americans today must have household income of $106,500 — up sharply from $59,000 just four years ago, according to Zillow research.

If lenders determine you are mortgage-worthy, they will then price your loan. Your credit score largely determines the mortgage rate you’ll get. A good affordability rule of thumb is to have three months of payments, including your housing payment and other monthly debts, in reserve. This will allow you to cover your mortgage payment in case of an unexpected event. However, as we explore below, there are a variety of programs to assist first-time buyers with down payments, closing costs, and financing.

Long-distance moves also incur additional expenses along the way, such as the cost of lodging, gas or airfare as you move from Point A to Point B. “Expert verified” means that our Financial Review Board thoroughly evaluated the article for accuracy and clarity. The Review Board comprises a panel of financial experts whose objective is to ensure that our content is always objective and balanced.

Mortgage insurance is a protection for the lender in case you ever cannot pay the loan back. If coming up with cash to pay for closing costs seems daunting, ask your lender about no-closing-cost options. Just keep in mind that doing so will cost you more in the long run, since you’ll be paying interest on the additional amount. Instead, take the time to research a few lenders and the different types of mortgage loans before applying. This extra step can ensure you have the best loan product and mortgage interest rate.

Can I Get a Mortgage With a Bad Credit Score?

Cost To Buy A House In Texas - Bankrate.com

Cost To Buy A House In Texas.

Posted: Wed, 29 Nov 2023 08:00:00 GMT [source]

Of course, these numbers can change drastically depending on your specific financial circumstances, including your homeowners insurance premium and local property taxes. If you lock in a lower rate, the monthly payments will be less; if you put down less than a 20 percent down payment, they will be more. Some homes may come with additional costs as well, such homeowners association fees or pool maintenance. Here’s everything you’ll want to consider to determine how much income is needed for a $400,000 home.

How Much Money Do You Need To Buy A House? FAQs

Many believe they need a 20% down payment to buy a house, but is that true? Let’s look at the actual data surrounding first-time home buyers and down payments. There are also more than 2,500 down payment assistance programs that can come in handy, especially if you’re a first-time homebuyer.

In general, you may qualify for a better interest rate with a higher down payment, which reduces the overall cost of your mortgage over time. Even a .25% reduction in your interest rate could save you thousands of dollars over the life of your loan. PMI will compensate the lender if the borrower defaults on the loan. In most cases, borrowers pay for PMI as a monthly premium that is added to their mortgage payment. The minimum down payment will largely depend on the type of loan you choose for your primary or secondary residence or investment property. You likely won’t put any money down if you qualify for a USDA or VA loan.

But on average, expect your closing costs to be an additional 2% to 5% of the loan amount. Your mortgage rate has a big impact on your monthly mortgage payment, which makes it crucial to shop with multiple lenders for the best mortgage rate. For example, if you got that same $240,000 loan at a 7.0 percent rate, the payment for monthly principal and interest increases to $1,596. However, it’s important to consider closing costs and other home-buying fees that you’ll need to pay for as well. That’s why you should speak with a professional mortgage expert or your real estate agent to make sure you’re making a down payment you can afford. Also referred to as the front-end ratio, this percentage represents the amount of your monthly income that goes towards housing expenses like your mortgage payment, insurance and taxes.

This influences which products we write about and where and how the product appears on a page.

Comments

Post a Comment